Truth #1-Past performance is no guarantee of future results.

Truth #2-The definition of insanity is doing the same thing over & over, and expecting a different result.

Are these two truths a paradox, or is one (or both) simply untrue? The answer is largely in the semantics, as is often the case. Although past performance does not guarantee future results, doing the same thing repeatedly rarely generates different results (most other things equal).

Once I was discussing personal finance with a friend who questioned the benefits of setting money aside for the future with "what if you die early?" To which I sharply responded, "what if you don't?!" As I have discussed before, "what if" can be a precarious game that portends mistakes.

The drivers of personal finance are uncertainty and probabilities. Over time, stocks generally return better performance than bonds or cash equivalents. Likewise, human generally live 80 years. Neither generality ensures that stocks will outperform bonds and cash in any given year any more than it can ensure survival through the year. Regardless, if stocks outperform bonds and cash seven of every 10 years with higher average annual performance for each period, then expecting stocks to outperform bonds and cash over the long run is highly reasonable (the opposite of insanity).

Even when expectations change, it is generally best to stay the course, at least until the changes become more certain. Several years ago, I was talking to a friend about an obligatory market recession because the bull run had been going for so long. She referred me to a source, citing that the man had been projecting this downturn for the past five years, to which I quipped "So, he has been wrong for the past five years." She quickly defended him, before realizing what I had said was in fact true. That bull market has continued fairly strongly through today as the Dow Jones has 30,000 on the horizon.

Until domestic stocks prove to be unreliable performers, they are the best foundation of a growth portfolio for the next 10 year or more. Perhaps decades from now, international stocks will have proven to outperform domestic stocks significantly more often than not, in which case they may become a better foundation for growth portfolios. But projecting that shift today and shorting domestic stocks as a result has not been a reasonable strategy.

Saturday, February 22, 2020

Monday, February 10, 2020

The Full Motley -- 1Q, 2020

Another anniversary entry today, starting my 11th year of financial blogging. In that time, I have gone from the recordkeeping department of a finance company to community college for a Paralegal Studies Program into work at a small bankruptcy firm to the legal department of a finance company. During this time, I have been contributing to my Roth IRA and my 401(k) accounts when available (too bad I missed out on that misunderstood myRA by a few months).

There were a couple years though that I did not max out my Roth IRA. Honestly, I did not even contribute to my Roth IRA for that year I was in school. Why? Due to those personal circumstances.

I have been of the mindset lately that financial bloggers need to put more emphasis on the “personal” in personal finance. It is misleading to promote personal finance as a series of rules to follow. Those rules are guidelines or self-discipline, adjustable to circumstances. I have been fortunate enough to max out my Roth IRA for many years, but when financial bloggers say to “max out your IRA,” people think “I cannot reach the max, so that advice won’t do any good.” The end result is a step in the wrong direction. Contributing half of the maximum amount would still be progress in the right direction (with the ultimate destination being financial security). I would love to hear that advice worded as “Contribute to your Roth IRA, maxing it out when you can.” That advice not only supports starting with smaller amounts, but even places that as an expected starting place. It is rare that someone has the financial freedom to adjust their finances immediately. Most have to not only learn good habits but also break their bad habits, and those steps may not happen concurrently.

My quarterly reallocations are almost always moving small percentages. This move saw about 0.7% of the account moving into domestic bonds and international equities, taken predominantly from the domestic equities and a sliver from international bonds. Although it was less than 1% of the account balance, the dollar amount equating 1% has risen significantly over the past 11 years because the account balance has almost tripled since April 30, 2011. There have been no new contributions since that time, and recently, I even learned that my employer put more money into this account than I did. The amount I set aside was not even a large amount (about the sum of my annual income when I was first hired there). Regardless, this account is currently the single largest portfolio of my net worth today.

Patience is a virtue, and patience pays, especially in the stock market. I have my own first hand testament to it, but I read an interview with John Hancock’s Retirement Plan Services CEO Patrick Murphy recently, and I wanted to share it because it is another voice saying what I have for years. His words rang more powerful to me, in large part through his current position and dismal early-life circumstances. (The following comes from Emily Laermer and some of his responses were edited for brevity and clarity by Ignites.)

Q: How did you get into the industry?

I got into this business not to help people accumulate wealth, but to help people avoid becoming poor.

I’m one of six kids. My parents got divorced when I was young, and then my dad died. He left us no life insurance, no savings, no nothing. My mom was left with six kids, and we had to figure out how to fend for ourselves. And we lived on welfare for a long time.

Fast forward, I muddle my way through high school, I get the opportunity to play college football and get an education. And then I took an economics class, and I learned about financial services. And I realized that what happened to my family never has to happen to anybody. It’s tragic enough to lose a parent and a bread-winner, but then to be plunged into poverty because of a lack of planning? That was a big, "aha!" moment for me.

I’m a big believer in the power of financial security. You can break the cycle of poverty by helping people acquire the skills and the habits.

Q: How do you get investors to actually start saving money?

Sometimes I tell them my story. I’m living proof that this stuff actually works — and it works well.

I started saving when I was 22 years old. It’s a real basic formula. Everybody’s trying to figure out how to time the market and how to outsmart the system. It’s not really that complex. I tell them to start early, save as much as they can and then increase over time. Then, just invest wisely.

Q: What plan design features tend to work best?

I’m a big believer in auto features. It’s not that people are stupid; people are nervous and stressed. That creates inaction.

If we can just auto enroll them and auto escalate them, and provide auto advice, then people eventually start to really engage. Then they get confidence, and then they start to learn more, and then they become more proficient. But trying to do all that up front is hard.

Q: You’ve been in the industry for over 30 years. What change has had the biggest impact?

Technology. Previously, it was really people-intensive labor to provide the kinds of services to participants that we can provide now. Now, it’s easy, scalable and cost effective to provide the level of real personalized service that was so expensive and cumbersome 30 years ago.

Now you can provide a better experience for the customer with greater levels of compliance. And quality and accuracy are more cost-effective. We can actually serve more people in a higher-quality way and run a profitable business at the same time.

Q: What trends will most impact the industry in the next decade?

The HSA market is really interesting. Health care is a big competing cost for companies and for employees, as it relates to what prevents them from saving for retirement.

HSAs are a way to invest for future health care costs. A lot of people today use them as a pass-through to pay for current-year medical expenses. But they are also a really powerful tool to help address a growing need in retirement.

What people forget is that their medical expenses might not be that high when they first retire, but their leisure expenses will be really high. And then later, that kind of flips. So they don’t really travel as much, but their health care expenses increase.

Q: What is the biggest challenge facing the retirement industry?

It’s helping customers understand the value that we provide. We’re in an era of fee compression, where everybody wants the lowest-cost thing. And everybody’s like, "Cheaper is better."

Cheaper is not better.

What adds value is helping customers understand the value that we provide to them.

Contact the reporter on this story at elaermer@ignites.com or (212) 542-1226.

Link:https://www.ignites.com/c/2635223/319293/living_proof_that_this_stuff_actually_works_hancock_retirement_chief

There were a couple years though that I did not max out my Roth IRA. Honestly, I did not even contribute to my Roth IRA for that year I was in school. Why? Due to those personal circumstances.

I have been of the mindset lately that financial bloggers need to put more emphasis on the “personal” in personal finance. It is misleading to promote personal finance as a series of rules to follow. Those rules are guidelines or self-discipline, adjustable to circumstances. I have been fortunate enough to max out my Roth IRA for many years, but when financial bloggers say to “max out your IRA,” people think “I cannot reach the max, so that advice won’t do any good.” The end result is a step in the wrong direction. Contributing half of the maximum amount would still be progress in the right direction (with the ultimate destination being financial security). I would love to hear that advice worded as “Contribute to your Roth IRA, maxing it out when you can.” That advice not only supports starting with smaller amounts, but even places that as an expected starting place. It is rare that someone has the financial freedom to adjust their finances immediately. Most have to not only learn good habits but also break their bad habits, and those steps may not happen concurrently.

My quarterly reallocations are almost always moving small percentages. This move saw about 0.7% of the account moving into domestic bonds and international equities, taken predominantly from the domestic equities and a sliver from international bonds. Although it was less than 1% of the account balance, the dollar amount equating 1% has risen significantly over the past 11 years because the account balance has almost tripled since April 30, 2011. There have been no new contributions since that time, and recently, I even learned that my employer put more money into this account than I did. The amount I set aside was not even a large amount (about the sum of my annual income when I was first hired there). Regardless, this account is currently the single largest portfolio of my net worth today.

Patience is a virtue, and patience pays, especially in the stock market. I have my own first hand testament to it, but I read an interview with John Hancock’s Retirement Plan Services CEO Patrick Murphy recently, and I wanted to share it because it is another voice saying what I have for years. His words rang more powerful to me, in large part through his current position and dismal early-life circumstances. (The following comes from Emily Laermer and some of his responses were edited for brevity and clarity by Ignites.)

Q: How did you get into the industry?

I got into this business not to help people accumulate wealth, but to help people avoid becoming poor.

I’m one of six kids. My parents got divorced when I was young, and then my dad died. He left us no life insurance, no savings, no nothing. My mom was left with six kids, and we had to figure out how to fend for ourselves. And we lived on welfare for a long time.

Fast forward, I muddle my way through high school, I get the opportunity to play college football and get an education. And then I took an economics class, and I learned about financial services. And I realized that what happened to my family never has to happen to anybody. It’s tragic enough to lose a parent and a bread-winner, but then to be plunged into poverty because of a lack of planning? That was a big, "aha!" moment for me.

I’m a big believer in the power of financial security. You can break the cycle of poverty by helping people acquire the skills and the habits.

Q: How do you get investors to actually start saving money?

Sometimes I tell them my story. I’m living proof that this stuff actually works — and it works well.

I started saving when I was 22 years old. It’s a real basic formula. Everybody’s trying to figure out how to time the market and how to outsmart the system. It’s not really that complex. I tell them to start early, save as much as they can and then increase over time. Then, just invest wisely.

Q: What plan design features tend to work best?

I’m a big believer in auto features. It’s not that people are stupid; people are nervous and stressed. That creates inaction.

If we can just auto enroll them and auto escalate them, and provide auto advice, then people eventually start to really engage. Then they get confidence, and then they start to learn more, and then they become more proficient. But trying to do all that up front is hard.

Q: You’ve been in the industry for over 30 years. What change has had the biggest impact?

Technology. Previously, it was really people-intensive labor to provide the kinds of services to participants that we can provide now. Now, it’s easy, scalable and cost effective to provide the level of real personalized service that was so expensive and cumbersome 30 years ago.

Now you can provide a better experience for the customer with greater levels of compliance. And quality and accuracy are more cost-effective. We can actually serve more people in a higher-quality way and run a profitable business at the same time.

Q: What trends will most impact the industry in the next decade?

The HSA market is really interesting. Health care is a big competing cost for companies and for employees, as it relates to what prevents them from saving for retirement.

HSAs are a way to invest for future health care costs. A lot of people today use them as a pass-through to pay for current-year medical expenses. But they are also a really powerful tool to help address a growing need in retirement.

What people forget is that their medical expenses might not be that high when they first retire, but their leisure expenses will be really high. And then later, that kind of flips. So they don’t really travel as much, but their health care expenses increase.

Q: What is the biggest challenge facing the retirement industry?

It’s helping customers understand the value that we provide. We’re in an era of fee compression, where everybody wants the lowest-cost thing. And everybody’s like, "Cheaper is better."

Cheaper is not better.

What adds value is helping customers understand the value that we provide to them.

Contact the reporter on this story at elaermer@ignites.com or (212) 542-1226.

Link:https://www.ignites.com/c/2635223/319293/living_proof_that_this_stuff_actually_works_hancock_retirement_chief

Thursday, November 14, 2019

The Full Motley -- 4Q, 2019

What a difference a year makes! Hopefully anyway. Last year, the fourth quarter was not terribly worrisome, until its Christmas Eve Massacre of 2018. No direct casualties, but markets plummeted on an otherwise historically light trading day. The Dow erased 12.5% of its previous highs at the end of 2018. Overall, the markets are now nearing a 20% return for the current year. Fantastic returns, but comparing the 2018 high (26,828) to 2019 high so far (27,782) is a more tempered 3.5%.

Herein lies the folly of performance reports; even when factually supported, true numbers. Some say number don’t lie. Ultimately that is untrue because numbers are just words, and we all know that words can lie. Performance chasing may not be as lucrative as the uninitiated would perceive either. Not every strong performance is the start of a trend. It is about as predictive of future success as an academy award. Sometimes, a surprise Actor of the Year winner enjoys a prolific career after an award-winning break-out performance. But not reliably so.

Instead of get-rich-quick, the slow-and-steady approach wins the race. Setting a comfortable asset allocation with disciplined reallocations create the groundwork for reliable success in the markets. This quarter, my reallocation removed about 1% from Total Bond Market Index Fund, not surprisingly after the Federal Reserve Board opted to lower interest rates even further earlier in the quarter, creating a higher demand for existing bonds (as well as removing downward pressure on existing bonds that comes when interest rates rise). Those assets were then placed into the International Stock Market Index Fund, which was down considerably through a concoction of global market woes in almost every developed country.

Herein lies the folly of performance reports; even when factually supported, true numbers. Some say number don’t lie. Ultimately that is untrue because numbers are just words, and we all know that words can lie. Performance chasing may not be as lucrative as the uninitiated would perceive either. Not every strong performance is the start of a trend. It is about as predictive of future success as an academy award. Sometimes, a surprise Actor of the Year winner enjoys a prolific career after an award-winning break-out performance. But not reliably so.

Instead of get-rich-quick, the slow-and-steady approach wins the race. Setting a comfortable asset allocation with disciplined reallocations create the groundwork for reliable success in the markets. This quarter, my reallocation removed about 1% from Total Bond Market Index Fund, not surprisingly after the Federal Reserve Board opted to lower interest rates even further earlier in the quarter, creating a higher demand for existing bonds (as well as removing downward pressure on existing bonds that comes when interest rates rise). Those assets were then placed into the International Stock Market Index Fund, which was down considerably through a concoction of global market woes in almost every developed country.

Sunday, September 29, 2019

Another Inconvenient Truth

Have you ever noticed that the prices of items at a convenient store are significantly more expensive than identical items at a grocery store? Have you ever noticed that, although it is a one-stop shop, the size of a Walmart Supercenters is 175,000 sq. ft. on average? We know that the rich get richer and the poor get poorer, but there are very few identifiable expenses that explain the difference.

One reason is convenience charges. Unlike buying tickets off Ticketmaster or other online retailers, where “convenience charge” appears on the itemized receipt, most convenience charges are explained only by strange pricing differentials. Your closest convenience store is not going to sell as many gallons of milk as your grocer for a couple reasons. One, because the price of milk is more expensive at the convenience store. Two, because there are so many more convenience stores than grocers. Whether one is a chicken and the other is an egg, I do not know. But a convenience store will earn more on each unit of milk sold – while a grocer will have lower margins and a higher volume of sales.

Why buy from a convenience store, instead of your grocer? There is no discernible reason to, unless you just like paying more (which, arguably would be the opposite of reasonable, as the I-didn’t-pay-enough tax fund in Arizona has proven). Except, there is a matter of convenience.

It is easier to drive a block to the closest convenience store to buy milk than to go to your local grocer or even a Walmart Supercenter. The building is smaller, so everything is closer together. The higher prices limit the number of customers, so there is no wait. You can get a gallon of milk in five minutes from a convenience store, or you can spend 20 minutes going to Walmart and back. Time is money, so there are people willing to pay for convenience.

Your pizza order is going to be subject to a delivery charge if you have it brought to you. (Ditto for Grubhub, UberEats, Postmates, and the like.) We know them as a delivery charge. A convenience charge by any other name would still reach as high.

What is the problem with convenience charges then? They become very expensive if you do not realize when you are paying them. If you cannot be bothered to leave your home for a meal, and you want fast-food instead of preparing something at your house, then you have every right to order delivery – but it comes at a price. You could have saved more by slightly “inconveniencing” yourself, either by planning ahead and stocking cupboards with easy meals or by stopping at a drive-through before coming home.

The great debate among people who say that they never splurge is when they rack up these expenses repeatedly – daily, even multiple times a day. Not being aware of how much more you pay than you should does not mean it does not exist. When the counterpart of the debate say they are living below their means, this is a big part of what they mean. They can afford convenience charges, but they opt for more inconvenient options to avoid them. They can afford bigger homes or nicer cars, but they transfer the benefits obtained from those purchases and redirect it elsewhere, most likely into their own wealth accumulation. I remember going to lunch with a friend of mine who had a (quite frankly) surprisingly nice car! I told him how great his car looked, to which his kneejerk reply was, “thanks, I’m not sure it is worth how much I pay for it.”

There are conveniences that come with a nice car, to be sure, but whether the sum of those conveniences match the price is another issue. The hidden expenses of a nicer car, including the higher quality tires and more expensive repairs and maintenance, add up subtly.

One reason is convenience charges. Unlike buying tickets off Ticketmaster or other online retailers, where “convenience charge” appears on the itemized receipt, most convenience charges are explained only by strange pricing differentials. Your closest convenience store is not going to sell as many gallons of milk as your grocer for a couple reasons. One, because the price of milk is more expensive at the convenience store. Two, because there are so many more convenience stores than grocers. Whether one is a chicken and the other is an egg, I do not know. But a convenience store will earn more on each unit of milk sold – while a grocer will have lower margins and a higher volume of sales.

Why buy from a convenience store, instead of your grocer? There is no discernible reason to, unless you just like paying more (which, arguably would be the opposite of reasonable, as the I-didn’t-pay-enough tax fund in Arizona has proven). Except, there is a matter of convenience.

It is easier to drive a block to the closest convenience store to buy milk than to go to your local grocer or even a Walmart Supercenter. The building is smaller, so everything is closer together. The higher prices limit the number of customers, so there is no wait. You can get a gallon of milk in five minutes from a convenience store, or you can spend 20 minutes going to Walmart and back. Time is money, so there are people willing to pay for convenience.

Your pizza order is going to be subject to a delivery charge if you have it brought to you. (Ditto for Grubhub, UberEats, Postmates, and the like.) We know them as a delivery charge. A convenience charge by any other name would still reach as high.

What is the problem with convenience charges then? They become very expensive if you do not realize when you are paying them. If you cannot be bothered to leave your home for a meal, and you want fast-food instead of preparing something at your house, then you have every right to order delivery – but it comes at a price. You could have saved more by slightly “inconveniencing” yourself, either by planning ahead and stocking cupboards with easy meals or by stopping at a drive-through before coming home.

The great debate among people who say that they never splurge is when they rack up these expenses repeatedly – daily, even multiple times a day. Not being aware of how much more you pay than you should does not mean it does not exist. When the counterpart of the debate say they are living below their means, this is a big part of what they mean. They can afford convenience charges, but they opt for more inconvenient options to avoid them. They can afford bigger homes or nicer cars, but they transfer the benefits obtained from those purchases and redirect it elsewhere, most likely into their own wealth accumulation. I remember going to lunch with a friend of mine who had a (quite frankly) surprisingly nice car! I told him how great his car looked, to which his kneejerk reply was, “thanks, I’m not sure it is worth how much I pay for it.”

There are conveniences that come with a nice car, to be sure, but whether the sum of those conveniences match the price is another issue. The hidden expenses of a nicer car, including the higher quality tires and more expensive repairs and maintenance, add up subtly.

Saturday, September 14, 2019

Indexing Made Easy - But Too Easy?

Indexing is easy. As I (and others) have said repeatedly. That simplicity could be its biggest drawback based on people's confirmation bias that finance is risky or at least tricky. People who want to believe that there is a good reason why they are not investing will believe those who say index returns are average returns. In reality, active management is a zero-sum game so for every dollar earned over the index return is at the expense of a dollar under-performing the market. While it is often simplified as saying "for every winner, there is a loser," and therefore index returns would be average, the reality is that the "winning" dollars are often disproportionately distributed, and there are several people losing a few dollars to a few winners claiming a lot of dollars. Just behind the returns of those few winners are the returns of index funds.

This week, I saw that Jim Cramer had touted the benefit of index investing, but upon further research, this latest claim was not the first time he had said as much. Even back in June 2014, he must have made similar statements because I found an article from MarketWatch's Retirementors recording the statement. That article is reprinted in full below, along with an interesting reader comment that warrants further discussion.

Jim Cramer likes index funds — Who knew?

https://www.marketwatch.com/story/jim-cramer-likes-index-funds-who-knew-2014-06-26

By Mitch Tuchman

Jim Cramer, the "Mad Money" cable TV host known for using his perch to preach stock-picking to the masses, has a simple message for retirement investors: Don't buy stock-picking mutual funds.

Yes, he still believes that picking stocks is time well-spent for some, but in a recent episode of his hugely popular show, Cramer launched into a tirade against the stock-picking industry, at least as it's sold to retail investors via actively managed funds. And he unabashedly supported owning low-cost, simple index funds in their place. in their place.

"If you're investing in mutual funds you're most likely, well, to put it delicately — how about 'getting hosed,'" Cramer said.

The reason why is cost, Cramer explained. Mutual funds make money by increasing the number of dollars they manage. That means spending money to attract new investors.

A small number of active mutual funds can beat the market, but usually only barely and not by enough to offset the fees they must charge to advertise and draw in those new investors — their real business model.

"What they're being paid to do is bring in more money from you, from more investors," Cramer warned. "That's part of the reason why in study after study, year after year, it's shown that the actively managed mutual funds underperform the benchmarks."

Price of admission

The other problem is that mutual fund success, in the instances where it happens, tends over time to lose effectiveness.

"When a mutual fund delivers such great results for so long, if the manager is a decent guy or woman they'll stop accepting new investors because when a fund gets too big it becomes incredibly difficult to beat the market," Cramer pointed out.

Hold on to that thought for a moment. If the goal is to beat the market, and size makes it harder to do so, isn't the better option to instead own the whole market, to just own the index? Cramer thinks so.

An index fund thus becomes the world's best mutual fund, clearly the most consistently successful way to invest over time and one whose price of admission is extremely low.

That's the reason the SDPR S&P 500 exchange-traded fund SPY, -0.07%, which owns the Standard & Poor’s 500 Index SPX, -0.07%, has a $167 billion market cap, nearly triple the No. 2 ETF — which also happens to track the S&P 500, the iShares S&P 500 Index ETF IVV, -0.07%.

It's also the reason a range of indexing ETFs have gained such broad allegiance over the past decade. They and their index-fund brethren are cheap to own and they deliver the kind of drama-free return retirement investors seek.

Cramer has some negative things to say about the proliferation of exotic ETFs, and he's right. More choice isn't always better, as he points out. But he's also correct in arguing that there really are two kinds of investors: Those ready and willing to commit to being traders and to sweating the daily ins and outs of stock selection, and the rest of us.

A clear choice

For retirement investors, the choice increasingly is clear, Cramer contends.

"You want a cheap, low-cost index fund that mirrors the market as a whole, one that mimics the S&P 500. You have a vehicle that will let you participate in the strength of the market without spending the time picking individual stocks," he concluded. "This may sound like a really simple solution, but don't overthink it. The whole point of putting your money in the fund is to save you from time and effort to manage your own portfolio of stocks."

We agree with Cramer's general argument. We would add only that at least some retirement investors benefit from financial adviser guidance from time to time, and that owning a basket of index ETFs operating as a risk-adjusted portfolio is a better choice than a 100% stock portfolio, even if it is held as a single ETF. He likely would agree on both points.

Naturally, portfolio-quality ETFs can and should be absolutely minimal in terms of cost and minimalist in design. From there, simple rebalancing and cautious oversight are all you need to build and maintain an optimal long-term retirement plan.

Not new news, but for a man like Jim Cramer who has appeared on TV shows such as Arrested Development as his abrasive on-screen character, it is quite an endorsement for the merits of indexing. Of course, there are still deniers. People believe the Earth is flat, despite overwhelming evidence. People similarly believe indexing is inferior or flawed.

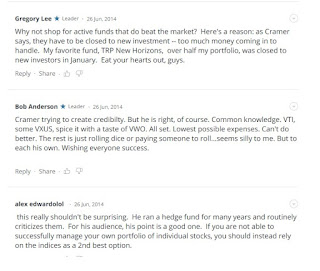

I enjoyed this comment, which was largely valid, that even the most successful actively managed funds have an unspoken disadvantage for investors where they tend to close to new investors so the portfolio managers can continue to manage them successfully without an onslaught of incoming assets. This investor noted T. Rowe Price New Horizon, which was closed to new investors after successfully outperforming the index.

I enjoyed this comment, which was largely valid, that even the most successful actively managed funds have an unspoken disadvantage for investors where they tend to close to new investors so the portfolio managers can continue to manage them successfully without an onslaught of incoming assets. This investor noted T. Rowe Price New Horizon, which was closed to new investors after successfully outperforming the index.

Pretty alluring. In June 2014, it was even an enviable position. If you had been forced to place money in Vanguard Total Stock Market Index Fund, instead of the closed TRP Fund, five years ago, then how would the returns have compared to opportunity cost of missing out on the TRP Fund? I ran a five-year comparison between the two funds on MarketWatch, and the results were amusing.

Investing $10,000 in the index fund back in September 2014, would have earned $54,100. Investing the same amount hypothetically into the TRP fund back in September 2014 would have earned $25,725.

This week, I saw that Jim Cramer had touted the benefit of index investing, but upon further research, this latest claim was not the first time he had said as much. Even back in June 2014, he must have made similar statements because I found an article from MarketWatch's Retirementors recording the statement. That article is reprinted in full below, along with an interesting reader comment that warrants further discussion.

Jim Cramer likes index funds — Who knew?

https://www.marketwatch.com/story/jim-cramer-likes-index-funds-who-knew-2014-06-26

By Mitch Tuchman

Jim Cramer, the "Mad Money" cable TV host known for using his perch to preach stock-picking to the masses, has a simple message for retirement investors: Don't buy stock-picking mutual funds.

Yes, he still believes that picking stocks is time well-spent for some, but in a recent episode of his hugely popular show, Cramer launched into a tirade against the stock-picking industry, at least as it's sold to retail investors via actively managed funds. And he unabashedly supported owning low-cost, simple index funds in their place. in their place.

"If you're investing in mutual funds you're most likely, well, to put it delicately — how about 'getting hosed,'" Cramer said.

The reason why is cost, Cramer explained. Mutual funds make money by increasing the number of dollars they manage. That means spending money to attract new investors.

A small number of active mutual funds can beat the market, but usually only barely and not by enough to offset the fees they must charge to advertise and draw in those new investors — their real business model.

"What they're being paid to do is bring in more money from you, from more investors," Cramer warned. "That's part of the reason why in study after study, year after year, it's shown that the actively managed mutual funds underperform the benchmarks."

Price of admission

The other problem is that mutual fund success, in the instances where it happens, tends over time to lose effectiveness.

"When a mutual fund delivers such great results for so long, if the manager is a decent guy or woman they'll stop accepting new investors because when a fund gets too big it becomes incredibly difficult to beat the market," Cramer pointed out.

Hold on to that thought for a moment. If the goal is to beat the market, and size makes it harder to do so, isn't the better option to instead own the whole market, to just own the index? Cramer thinks so.

An index fund thus becomes the world's best mutual fund, clearly the most consistently successful way to invest over time and one whose price of admission is extremely low.

That's the reason the SDPR S&P 500 exchange-traded fund SPY, -0.07%, which owns the Standard & Poor’s 500 Index SPX, -0.07%, has a $167 billion market cap, nearly triple the No. 2 ETF — which also happens to track the S&P 500, the iShares S&P 500 Index ETF IVV, -0.07%.

It's also the reason a range of indexing ETFs have gained such broad allegiance over the past decade. They and their index-fund brethren are cheap to own and they deliver the kind of drama-free return retirement investors seek.

Cramer has some negative things to say about the proliferation of exotic ETFs, and he's right. More choice isn't always better, as he points out. But he's also correct in arguing that there really are two kinds of investors: Those ready and willing to commit to being traders and to sweating the daily ins and outs of stock selection, and the rest of us.

A clear choice

For retirement investors, the choice increasingly is clear, Cramer contends.

"You want a cheap, low-cost index fund that mirrors the market as a whole, one that mimics the S&P 500. You have a vehicle that will let you participate in the strength of the market without spending the time picking individual stocks," he concluded. "This may sound like a really simple solution, but don't overthink it. The whole point of putting your money in the fund is to save you from time and effort to manage your own portfolio of stocks."

We agree with Cramer's general argument. We would add only that at least some retirement investors benefit from financial adviser guidance from time to time, and that owning a basket of index ETFs operating as a risk-adjusted portfolio is a better choice than a 100% stock portfolio, even if it is held as a single ETF. He likely would agree on both points.

Naturally, portfolio-quality ETFs can and should be absolutely minimal in terms of cost and minimalist in design. From there, simple rebalancing and cautious oversight are all you need to build and maintain an optimal long-term retirement plan.

Not new news, but for a man like Jim Cramer who has appeared on TV shows such as Arrested Development as his abrasive on-screen character, it is quite an endorsement for the merits of indexing. Of course, there are still deniers. People believe the Earth is flat, despite overwhelming evidence. People similarly believe indexing is inferior or flawed.

I enjoyed this comment, which was largely valid, that even the most successful actively managed funds have an unspoken disadvantage for investors where they tend to close to new investors so the portfolio managers can continue to manage them successfully without an onslaught of incoming assets. This investor noted T. Rowe Price New Horizon, which was closed to new investors after successfully outperforming the index.

I enjoyed this comment, which was largely valid, that even the most successful actively managed funds have an unspoken disadvantage for investors where they tend to close to new investors so the portfolio managers can continue to manage them successfully without an onslaught of incoming assets. This investor noted T. Rowe Price New Horizon, which was closed to new investors after successfully outperforming the index.Pretty alluring. In June 2014, it was even an enviable position. If you had been forced to place money in Vanguard Total Stock Market Index Fund, instead of the closed TRP Fund, five years ago, then how would the returns have compared to opportunity cost of missing out on the TRP Fund? I ran a five-year comparison between the two funds on MarketWatch, and the results were amusing.

Investing $10,000 in the index fund back in September 2014, would have earned $54,100. Investing the same amount hypothetically into the TRP fund back in September 2014 would have earned $25,725.

Saturday, August 17, 2019

The Full Motley – 3Q, 2019

I have been remiss in updating this blog since my 10th anniversary in February, but I have consistently been rebalancing quarterly. This week’s rebalance came amid a volatile week in the market. Losses of 800 points one day or gains of 500 points the next day evened out to end the week with a tolerable 300-point drop. Reactions to the daily volatility would be enough to convince market-watchers that big changes were occurring daily, but from a weekly view, those changes were rather minimal. This is the difference between investing for the short-term or investing for the long run. Our retirement investments are long-term investments. It is important to understand why (and how) the investments work, and that responsibility is falling to the individual – as many other things are as well.

This week, I was listening to a panel of Asian Americans speak about their cultural difference between their home countries (or origin countries, for those who were born here) and the United States, and a lot of the differences and obstacles that they identified sounded to be as much generational situations as cultural differences. The old way of succeeding was to keep quiet, keep your head down, and you would be rewarded for loyalty. The new way of succeeding is to carve out a path for yourself and you will be rewarded with opportunity.

Times are changing, in many ways – for better or worse. Among these changes, financial stability might have been one of the advantages lost in the shift away from "keep quiet and keep your head down" being sound advice. Just as workers are not rewarded for loyalty to companies; companies are not rewarded for loyalty to the workers. The idea of retirement pensions upon completion of a 40-year career with a single company is passe (both the pension, and the 40-year career with a single company). Now we speak up for ourselves. We assert our freedoms and individuality nowadays, but our financial stability was included in that shift. We can celebrate greater financial freedom now, but that requires taking the same approach of speaking up, asking questions and not keeping our heads down. Our financial success is up to us.

Investing in mutual funds spreads loyalty (the risks and rewards) to a single company by diversifying. Diversifying will mitigate the rewards when that company succeeds greatly, but it will limit the losses if the company fails. My investments are in the Vanguard Total Stock Market Index Fund, Vanguard PRIMECAP Fund, Vanguard Total International Stock Index Fund, Vanguard Bond Market Index Fund, and Vanguard Total International Bond Index Fund. These five investments provide me access to the global market, from domestic equities (both passive and active) to international equities, as well as domestic and international bonds. While I could diversify further with higher risk investments in alternative investments (such as real estate or commodities, including gold), I keep my 401k spread across the global marketplace and leave those investments for my individual accounts, such as my Roth IRA.

Interestingly, my rebalance for this quarter pulled from all assets to place into the Total International Stock Index Fund. That fund had been underperforming relative to the other funds in my account, but there are many strategic advantages to putting more money into that fund at this time, including the slowing American economy and/or the weakening American dollar will hit my largest funds the hardest. Whether the international index appreciates or just holds ground better, it is a good investment away from those investments that are most at-risk of those looming threats. If I read the headlines in the financial media (and I do), then I could become convinced that those threats are large and nearing. In a reactionary state of mind, I would pull more from those at-risk investments and shuffle the money into this international index. But much as the weekly market movement was relatively minor compared to the daily volatility seen, watching investments too closely can be hazardous to your wealth (and mental health). I will just endure what may come with my quarterly rebalancing. I am not convinced that any changes would be best in the long run, which is where I am truly invested.

This week, I was listening to a panel of Asian Americans speak about their cultural difference between their home countries (or origin countries, for those who were born here) and the United States, and a lot of the differences and obstacles that they identified sounded to be as much generational situations as cultural differences. The old way of succeeding was to keep quiet, keep your head down, and you would be rewarded for loyalty. The new way of succeeding is to carve out a path for yourself and you will be rewarded with opportunity.

Times are changing, in many ways – for better or worse. Among these changes, financial stability might have been one of the advantages lost in the shift away from "keep quiet and keep your head down" being sound advice. Just as workers are not rewarded for loyalty to companies; companies are not rewarded for loyalty to the workers. The idea of retirement pensions upon completion of a 40-year career with a single company is passe (both the pension, and the 40-year career with a single company). Now we speak up for ourselves. We assert our freedoms and individuality nowadays, but our financial stability was included in that shift. We can celebrate greater financial freedom now, but that requires taking the same approach of speaking up, asking questions and not keeping our heads down. Our financial success is up to us.

Investing in mutual funds spreads loyalty (the risks and rewards) to a single company by diversifying. Diversifying will mitigate the rewards when that company succeeds greatly, but it will limit the losses if the company fails. My investments are in the Vanguard Total Stock Market Index Fund, Vanguard PRIMECAP Fund, Vanguard Total International Stock Index Fund, Vanguard Bond Market Index Fund, and Vanguard Total International Bond Index Fund. These five investments provide me access to the global market, from domestic equities (both passive and active) to international equities, as well as domestic and international bonds. While I could diversify further with higher risk investments in alternative investments (such as real estate or commodities, including gold), I keep my 401k spread across the global marketplace and leave those investments for my individual accounts, such as my Roth IRA.

Interestingly, my rebalance for this quarter pulled from all assets to place into the Total International Stock Index Fund. That fund had been underperforming relative to the other funds in my account, but there are many strategic advantages to putting more money into that fund at this time, including the slowing American economy and/or the weakening American dollar will hit my largest funds the hardest. Whether the international index appreciates or just holds ground better, it is a good investment away from those investments that are most at-risk of those looming threats. If I read the headlines in the financial media (and I do), then I could become convinced that those threats are large and nearing. In a reactionary state of mind, I would pull more from those at-risk investments and shuffle the money into this international index. But much as the weekly market movement was relatively minor compared to the daily volatility seen, watching investments too closely can be hazardous to your wealth (and mental health). I will just endure what may come with my quarterly rebalancing. I am not convinced that any changes would be best in the long run, which is where I am truly invested.

Sunday, February 10, 2019

The Full Motley -- 10 Year Anniversary (1Q, 2019)

No matter what age you are or which period you are tracking, ten years is a long time! As it is, ten years ago today was when I started tracking my 401(k) because the markets were about as low as I could imagine them, and I was so curious what was next. As it turned out, the markets would bottom out within a month and then begin on a record long bull run that did not end until December 2018. Basically, it was a 10-year period in which it was much harder to lose money than make money!

Regardless, a lot happened in that time: I quit my job, I went to school, I attempted to re-career from the finance industry into the legal field, I ended up in the legal department of a finance company, and I had to modify my 401(k) investments when my provider changed the investment options. As of today, I am also halfway through a M.B.A. program! Having worked in finance for 10 years though, this program feels more like it is papering down my knowledge base than brand new studies, which is not a bad thing.

My current ECON class textbook had an interesting take on active management versus indexing:

"Mutual fund investors have a choice between putting their money into actively managed mutual funds or into passively managed index funds. Actively managed funds constantly buy and sell assets in an attempt to build portfolios that will generate average expected rates of return that are higher than those of other portfolios possessing a similar level of risk. In terms of Figure 35.3, they try to construct portfolios similar to point A, which has the same level of risk as portfolio B but a much higher average expected rate of return. By contrast, the portfolios of index funds simply mimic the assets that are included in their underlying indexes and make no attempt whatsoever to generate higher returns than other portfolios having similar levels of risk.

"As a result, expecting actively managed funds to generate higher rates of return than index funds would seem only natural. Surprisingly, however, the exact opposite actually holds true. Once costs are taken into account, the average returns generated by index funds trounce those generated by actively managed funds by well over 1 percent per year. Now, 1 percent per year may not sound like a lot, but the compound interest formula of equation 1 shows that $10,000 growing for 30 years at 10 percent per year becomes $170,449.40, whereas that same amount of money growing at 11 percent for 30 years becomes $220,892.30. For anyone saving for retirement, an extra 1 percent per year is a very big deal.

"Why do actively managed funds do so much worse than index funds? The answer is twofold. First, arbitrage makes it virtually impossible for actively managed funds to select portfolios that will do any better than index funds that have similar levels of risk. As a result, before taking costs into account, actively managed funds and index funds produce very similar returns. Second, actively managed funds charge their investors much higher fees than do passively managed funds, so that, after taking costs into account, actively managed funds do worse by about 1 percent per year.

"Let us discuss each of these factors in more detail. The reason that actively managed funds cannot do better than index funds before taking costs into account has to do with the power of arbitrage to ensure that investments having equal levels of risk also have equal average expected rates of return. As we explained above with respect to Figure 35.3, assets and portfolios that deviate from the Security Market Line (SML) are very quickly forced back onto the SML by arbitrage, so that assets and portfolios with equal levels of risk have equal average expected rates of return. This implies that index funds and actively managed funds with equal levels of risk will end up with identical average expected rates of return despite the best efforts of actively managed funds to produce superior returns.

"The reason actively managed funds charge much higher fees than index funds is because they run up much higher costs while trying to produce superior returns. Not only do they have to pay large salaries to professional fund managers, but they also have to pay for the massive amounts of trading that those managers engage in as they buy and sell assets in their quest to produce superior returns. The costs of running an index fund are, by contrast, very small since changes are made to an index fund’s portfolio only on the rare occasions when the fund’s underlying index changes. As a result, trading costs are low and there is no need to pay for a professional manager. The overall result is that while the largest and most popular index fund currently charges its investors only 0.18 percent per year for its services, the typical actively managed fund charges more than 1.5 percent per year.

"So why are actively managed funds still in business? The answer may well be that index funds are boring. Because they are set up to mimic indexes that are in turn designed to show what average performance levels are, index funds are by definition stuck with average rates of return and absolutely no chance to exceed average rates of return. For investors who want to try to beat the average, actively managed funds are the only way to go."

Fairly rousing endorsement for what I have been following in the past 10+ years. Of course, the recurring question has been whether rebalancing quarterly has been too often, but this past quarter is a good example of its merits. On November 10, 2018, we had no idea what the next three months would be like! The markets were shaky, but a Christmas Eve Massacre saw the Dow plummet 650 points.

There were two ways to go: one, panic and make immediate changes or two, stay the course. In this case, staying my course involved weathering the fall for the next two months and then buying into the depleted markets by moving other assets that might have appreciated in that time. As it turned out, the market has recovered most of its losses since its recent lows, so staying the course was the best choice.

Therefore, my move for this rebalance was minor (as the past several have been). Instead of taking money from the stock funds though, this time I put money into those stock funds. Specifically, I took 1.5% from my International Stock Index Fund, 4.7% from my Bond Market Index Fund, and 4% from my International Bond Fund, and I placed that amount into my PRIMECAP Fund (53%) and my Total Stock Market Index Fund (47%). Nothing close to approaching 10%, but just like in baseball, winning in wealth creation is more about the consistent singles and doubles than the occasional home runs.

Regardless, a lot happened in that time: I quit my job, I went to school, I attempted to re-career from the finance industry into the legal field, I ended up in the legal department of a finance company, and I had to modify my 401(k) investments when my provider changed the investment options. As of today, I am also halfway through a M.B.A. program! Having worked in finance for 10 years though, this program feels more like it is papering down my knowledge base than brand new studies, which is not a bad thing.

My current ECON class textbook had an interesting take on active management versus indexing:

"Mutual fund investors have a choice between putting their money into actively managed mutual funds or into passively managed index funds. Actively managed funds constantly buy and sell assets in an attempt to build portfolios that will generate average expected rates of return that are higher than those of other portfolios possessing a similar level of risk. In terms of Figure 35.3, they try to construct portfolios similar to point A, which has the same level of risk as portfolio B but a much higher average expected rate of return. By contrast, the portfolios of index funds simply mimic the assets that are included in their underlying indexes and make no attempt whatsoever to generate higher returns than other portfolios having similar levels of risk.

"As a result, expecting actively managed funds to generate higher rates of return than index funds would seem only natural. Surprisingly, however, the exact opposite actually holds true. Once costs are taken into account, the average returns generated by index funds trounce those generated by actively managed funds by well over 1 percent per year. Now, 1 percent per year may not sound like a lot, but the compound interest formula of equation 1 shows that $10,000 growing for 30 years at 10 percent per year becomes $170,449.40, whereas that same amount of money growing at 11 percent for 30 years becomes $220,892.30. For anyone saving for retirement, an extra 1 percent per year is a very big deal.

"Why do actively managed funds do so much worse than index funds? The answer is twofold. First, arbitrage makes it virtually impossible for actively managed funds to select portfolios that will do any better than index funds that have similar levels of risk. As a result, before taking costs into account, actively managed funds and index funds produce very similar returns. Second, actively managed funds charge their investors much higher fees than do passively managed funds, so that, after taking costs into account, actively managed funds do worse by about 1 percent per year.

"Let us discuss each of these factors in more detail. The reason that actively managed funds cannot do better than index funds before taking costs into account has to do with the power of arbitrage to ensure that investments having equal levels of risk also have equal average expected rates of return. As we explained above with respect to Figure 35.3, assets and portfolios that deviate from the Security Market Line (SML) are very quickly forced back onto the SML by arbitrage, so that assets and portfolios with equal levels of risk have equal average expected rates of return. This implies that index funds and actively managed funds with equal levels of risk will end up with identical average expected rates of return despite the best efforts of actively managed funds to produce superior returns.

"The reason actively managed funds charge much higher fees than index funds is because they run up much higher costs while trying to produce superior returns. Not only do they have to pay large salaries to professional fund managers, but they also have to pay for the massive amounts of trading that those managers engage in as they buy and sell assets in their quest to produce superior returns. The costs of running an index fund are, by contrast, very small since changes are made to an index fund’s portfolio only on the rare occasions when the fund’s underlying index changes. As a result, trading costs are low and there is no need to pay for a professional manager. The overall result is that while the largest and most popular index fund currently charges its investors only 0.18 percent per year for its services, the typical actively managed fund charges more than 1.5 percent per year.

"So why are actively managed funds still in business? The answer may well be that index funds are boring. Because they are set up to mimic indexes that are in turn designed to show what average performance levels are, index funds are by definition stuck with average rates of return and absolutely no chance to exceed average rates of return. For investors who want to try to beat the average, actively managed funds are the only way to go."

Fairly rousing endorsement for what I have been following in the past 10+ years. Of course, the recurring question has been whether rebalancing quarterly has been too often, but this past quarter is a good example of its merits. On November 10, 2018, we had no idea what the next three months would be like! The markets were shaky, but a Christmas Eve Massacre saw the Dow plummet 650 points.

There were two ways to go: one, panic and make immediate changes or two, stay the course. In this case, staying my course involved weathering the fall for the next two months and then buying into the depleted markets by moving other assets that might have appreciated in that time. As it turned out, the market has recovered most of its losses since its recent lows, so staying the course was the best choice.

Therefore, my move for this rebalance was minor (as the past several have been). Instead of taking money from the stock funds though, this time I put money into those stock funds. Specifically, I took 1.5% from my International Stock Index Fund, 4.7% from my Bond Market Index Fund, and 4% from my International Bond Fund, and I placed that amount into my PRIMECAP Fund (53%) and my Total Stock Market Index Fund (47%). Nothing close to approaching 10%, but just like in baseball, winning in wealth creation is more about the consistent singles and doubles than the occasional home runs.

Subscribe to:

Posts (Atom)