Have you ever noticed that the prices of items at a convenient store are significantly more expensive than identical items at a grocery store? Have you ever noticed that, although it is a one-stop shop, the size of a Walmart Supercenters is 175,000 sq. ft. on average? We know that the rich get richer and the poor get poorer, but there are very few identifiable expenses that explain the difference.

One reason is convenience charges. Unlike buying tickets off Ticketmaster or other online retailers, where “convenience charge” appears on the itemized receipt, most convenience charges are explained only by strange pricing differentials. Your closest convenience store is not going to sell as many gallons of milk as your grocer for a couple reasons. One, because the price of milk is more expensive at the convenience store. Two, because there are so many more convenience stores than grocers. Whether one is a chicken and the other is an egg, I do not know. But a convenience store will earn more on each unit of milk sold – while a grocer will have lower margins and a higher volume of sales.

Why buy from a convenience store, instead of your grocer? There is no discernible reason to, unless you just like paying more (which, arguably would be the opposite of reasonable, as the I-didn’t-pay-enough tax fund in Arizona has proven). Except, there is a matter of convenience.

It is easier to drive a block to the closest convenience store to buy milk than to go to your local grocer or even a Walmart Supercenter. The building is smaller, so everything is closer together. The higher prices limit the number of customers, so there is no wait. You can get a gallon of milk in five minutes from a convenience store, or you can spend 20 minutes going to Walmart and back. Time is money, so there are people willing to pay for convenience.

Your pizza order is going to be subject to a delivery charge if you have it brought to you. (Ditto for Grubhub, UberEats, Postmates, and the like.) We know them as a delivery charge. A convenience charge by any other name would still reach as high.

What is the problem with convenience charges then? They become very expensive if you do not realize when you are paying them. If you cannot be bothered to leave your home for a meal, and you want fast-food instead of preparing something at your house, then you have every right to order delivery – but it comes at a price. You could have saved more by slightly “inconveniencing” yourself, either by planning ahead and stocking cupboards with easy meals or by stopping at a drive-through before coming home.

The great debate among people who say that they never splurge is when they rack up these expenses repeatedly – daily, even multiple times a day. Not being aware of how much more you pay than you should does not mean it does not exist. When the counterpart of the debate say they are living below their means, this is a big part of what they mean. They can afford convenience charges, but they opt for more inconvenient options to avoid them. They can afford bigger homes or nicer cars, but they transfer the benefits obtained from those purchases and redirect it elsewhere, most likely into their own wealth accumulation. I remember going to lunch with a friend of mine who had a (quite frankly) surprisingly nice car! I told him how great his car looked, to which his kneejerk reply was, “thanks, I’m not sure it is worth how much I pay for it.”

There are conveniences that come with a nice car, to be sure, but whether the sum of those conveniences match the price is another issue. The hidden expenses of a nicer car, including the higher quality tires and more expensive repairs and maintenance, add up subtly.

Sunday, September 29, 2019

Saturday, September 14, 2019

Indexing Made Easy - But Too Easy?

Indexing is easy. As I (and others) have said repeatedly. That simplicity could be its biggest drawback based on people's confirmation bias that finance is risky or at least tricky. People who want to believe that there is a good reason why they are not investing will believe those who say index returns are average returns. In reality, active management is a zero-sum game so for every dollar earned over the index return is at the expense of a dollar under-performing the market. While it is often simplified as saying "for every winner, there is a loser," and therefore index returns would be average, the reality is that the "winning" dollars are often disproportionately distributed, and there are several people losing a few dollars to a few winners claiming a lot of dollars. Just behind the returns of those few winners are the returns of index funds.

This week, I saw that Jim Cramer had touted the benefit of index investing, but upon further research, this latest claim was not the first time he had said as much. Even back in June 2014, he must have made similar statements because I found an article from MarketWatch's Retirementors recording the statement. That article is reprinted in full below, along with an interesting reader comment that warrants further discussion.

Jim Cramer likes index funds — Who knew?

https://www.marketwatch.com/story/jim-cramer-likes-index-funds-who-knew-2014-06-26

By Mitch Tuchman

Jim Cramer, the "Mad Money" cable TV host known for using his perch to preach stock-picking to the masses, has a simple message for retirement investors: Don't buy stock-picking mutual funds.

Yes, he still believes that picking stocks is time well-spent for some, but in a recent episode of his hugely popular show, Cramer launched into a tirade against the stock-picking industry, at least as it's sold to retail investors via actively managed funds. And he unabashedly supported owning low-cost, simple index funds in their place. in their place.

"If you're investing in mutual funds you're most likely, well, to put it delicately — how about 'getting hosed,'" Cramer said.

The reason why is cost, Cramer explained. Mutual funds make money by increasing the number of dollars they manage. That means spending money to attract new investors.

A small number of active mutual funds can beat the market, but usually only barely and not by enough to offset the fees they must charge to advertise and draw in those new investors — their real business model.

"What they're being paid to do is bring in more money from you, from more investors," Cramer warned. "That's part of the reason why in study after study, year after year, it's shown that the actively managed mutual funds underperform the benchmarks."

Price of admission

The other problem is that mutual fund success, in the instances where it happens, tends over time to lose effectiveness.

"When a mutual fund delivers such great results for so long, if the manager is a decent guy or woman they'll stop accepting new investors because when a fund gets too big it becomes incredibly difficult to beat the market," Cramer pointed out.

Hold on to that thought for a moment. If the goal is to beat the market, and size makes it harder to do so, isn't the better option to instead own the whole market, to just own the index? Cramer thinks so.

An index fund thus becomes the world's best mutual fund, clearly the most consistently successful way to invest over time and one whose price of admission is extremely low.

That's the reason the SDPR S&P 500 exchange-traded fund SPY, -0.07%, which owns the Standard & Poor’s 500 Index SPX, -0.07%, has a $167 billion market cap, nearly triple the No. 2 ETF — which also happens to track the S&P 500, the iShares S&P 500 Index ETF IVV, -0.07%.

It's also the reason a range of indexing ETFs have gained such broad allegiance over the past decade. They and their index-fund brethren are cheap to own and they deliver the kind of drama-free return retirement investors seek.

Cramer has some negative things to say about the proliferation of exotic ETFs, and he's right. More choice isn't always better, as he points out. But he's also correct in arguing that there really are two kinds of investors: Those ready and willing to commit to being traders and to sweating the daily ins and outs of stock selection, and the rest of us.

A clear choice

For retirement investors, the choice increasingly is clear, Cramer contends.

"You want a cheap, low-cost index fund that mirrors the market as a whole, one that mimics the S&P 500. You have a vehicle that will let you participate in the strength of the market without spending the time picking individual stocks," he concluded. "This may sound like a really simple solution, but don't overthink it. The whole point of putting your money in the fund is to save you from time and effort to manage your own portfolio of stocks."

We agree with Cramer's general argument. We would add only that at least some retirement investors benefit from financial adviser guidance from time to time, and that owning a basket of index ETFs operating as a risk-adjusted portfolio is a better choice than a 100% stock portfolio, even if it is held as a single ETF. He likely would agree on both points.

Naturally, portfolio-quality ETFs can and should be absolutely minimal in terms of cost and minimalist in design. From there, simple rebalancing and cautious oversight are all you need to build and maintain an optimal long-term retirement plan.

Not new news, but for a man like Jim Cramer who has appeared on TV shows such as Arrested Development as his abrasive on-screen character, it is quite an endorsement for the merits of indexing. Of course, there are still deniers. People believe the Earth is flat, despite overwhelming evidence. People similarly believe indexing is inferior or flawed.

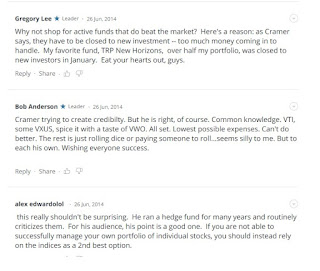

I enjoyed this comment, which was largely valid, that even the most successful actively managed funds have an unspoken disadvantage for investors where they tend to close to new investors so the portfolio managers can continue to manage them successfully without an onslaught of incoming assets. This investor noted T. Rowe Price New Horizon, which was closed to new investors after successfully outperforming the index.

I enjoyed this comment, which was largely valid, that even the most successful actively managed funds have an unspoken disadvantage for investors where they tend to close to new investors so the portfolio managers can continue to manage them successfully without an onslaught of incoming assets. This investor noted T. Rowe Price New Horizon, which was closed to new investors after successfully outperforming the index.

Pretty alluring. In June 2014, it was even an enviable position. If you had been forced to place money in Vanguard Total Stock Market Index Fund, instead of the closed TRP Fund, five years ago, then how would the returns have compared to opportunity cost of missing out on the TRP Fund? I ran a five-year comparison between the two funds on MarketWatch, and the results were amusing.

Investing $10,000 in the index fund back in September 2014, would have earned $54,100. Investing the same amount hypothetically into the TRP fund back in September 2014 would have earned $25,725.

This week, I saw that Jim Cramer had touted the benefit of index investing, but upon further research, this latest claim was not the first time he had said as much. Even back in June 2014, he must have made similar statements because I found an article from MarketWatch's Retirementors recording the statement. That article is reprinted in full below, along with an interesting reader comment that warrants further discussion.

Jim Cramer likes index funds — Who knew?

https://www.marketwatch.com/story/jim-cramer-likes-index-funds-who-knew-2014-06-26

By Mitch Tuchman

Jim Cramer, the "Mad Money" cable TV host known for using his perch to preach stock-picking to the masses, has a simple message for retirement investors: Don't buy stock-picking mutual funds.

Yes, he still believes that picking stocks is time well-spent for some, but in a recent episode of his hugely popular show, Cramer launched into a tirade against the stock-picking industry, at least as it's sold to retail investors via actively managed funds. And he unabashedly supported owning low-cost, simple index funds in their place. in their place.

"If you're investing in mutual funds you're most likely, well, to put it delicately — how about 'getting hosed,'" Cramer said.

The reason why is cost, Cramer explained. Mutual funds make money by increasing the number of dollars they manage. That means spending money to attract new investors.

A small number of active mutual funds can beat the market, but usually only barely and not by enough to offset the fees they must charge to advertise and draw in those new investors — their real business model.

"What they're being paid to do is bring in more money from you, from more investors," Cramer warned. "That's part of the reason why in study after study, year after year, it's shown that the actively managed mutual funds underperform the benchmarks."

Price of admission

The other problem is that mutual fund success, in the instances where it happens, tends over time to lose effectiveness.

"When a mutual fund delivers such great results for so long, if the manager is a decent guy or woman they'll stop accepting new investors because when a fund gets too big it becomes incredibly difficult to beat the market," Cramer pointed out.

Hold on to that thought for a moment. If the goal is to beat the market, and size makes it harder to do so, isn't the better option to instead own the whole market, to just own the index? Cramer thinks so.

An index fund thus becomes the world's best mutual fund, clearly the most consistently successful way to invest over time and one whose price of admission is extremely low.

That's the reason the SDPR S&P 500 exchange-traded fund SPY, -0.07%, which owns the Standard & Poor’s 500 Index SPX, -0.07%, has a $167 billion market cap, nearly triple the No. 2 ETF — which also happens to track the S&P 500, the iShares S&P 500 Index ETF IVV, -0.07%.

It's also the reason a range of indexing ETFs have gained such broad allegiance over the past decade. They and their index-fund brethren are cheap to own and they deliver the kind of drama-free return retirement investors seek.

Cramer has some negative things to say about the proliferation of exotic ETFs, and he's right. More choice isn't always better, as he points out. But he's also correct in arguing that there really are two kinds of investors: Those ready and willing to commit to being traders and to sweating the daily ins and outs of stock selection, and the rest of us.

A clear choice

For retirement investors, the choice increasingly is clear, Cramer contends.

"You want a cheap, low-cost index fund that mirrors the market as a whole, one that mimics the S&P 500. You have a vehicle that will let you participate in the strength of the market without spending the time picking individual stocks," he concluded. "This may sound like a really simple solution, but don't overthink it. The whole point of putting your money in the fund is to save you from time and effort to manage your own portfolio of stocks."

We agree with Cramer's general argument. We would add only that at least some retirement investors benefit from financial adviser guidance from time to time, and that owning a basket of index ETFs operating as a risk-adjusted portfolio is a better choice than a 100% stock portfolio, even if it is held as a single ETF. He likely would agree on both points.

Naturally, portfolio-quality ETFs can and should be absolutely minimal in terms of cost and minimalist in design. From there, simple rebalancing and cautious oversight are all you need to build and maintain an optimal long-term retirement plan.

Not new news, but for a man like Jim Cramer who has appeared on TV shows such as Arrested Development as his abrasive on-screen character, it is quite an endorsement for the merits of indexing. Of course, there are still deniers. People believe the Earth is flat, despite overwhelming evidence. People similarly believe indexing is inferior or flawed.

I enjoyed this comment, which was largely valid, that even the most successful actively managed funds have an unspoken disadvantage for investors where they tend to close to new investors so the portfolio managers can continue to manage them successfully without an onslaught of incoming assets. This investor noted T. Rowe Price New Horizon, which was closed to new investors after successfully outperforming the index.

I enjoyed this comment, which was largely valid, that even the most successful actively managed funds have an unspoken disadvantage for investors where they tend to close to new investors so the portfolio managers can continue to manage them successfully without an onslaught of incoming assets. This investor noted T. Rowe Price New Horizon, which was closed to new investors after successfully outperforming the index.Pretty alluring. In June 2014, it was even an enviable position. If you had been forced to place money in Vanguard Total Stock Market Index Fund, instead of the closed TRP Fund, five years ago, then how would the returns have compared to opportunity cost of missing out on the TRP Fund? I ran a five-year comparison between the two funds on MarketWatch, and the results were amusing.

Investing $10,000 in the index fund back in September 2014, would have earned $54,100. Investing the same amount hypothetically into the TRP fund back in September 2014 would have earned $25,725.

Subscribe to:

Comments (Atom)